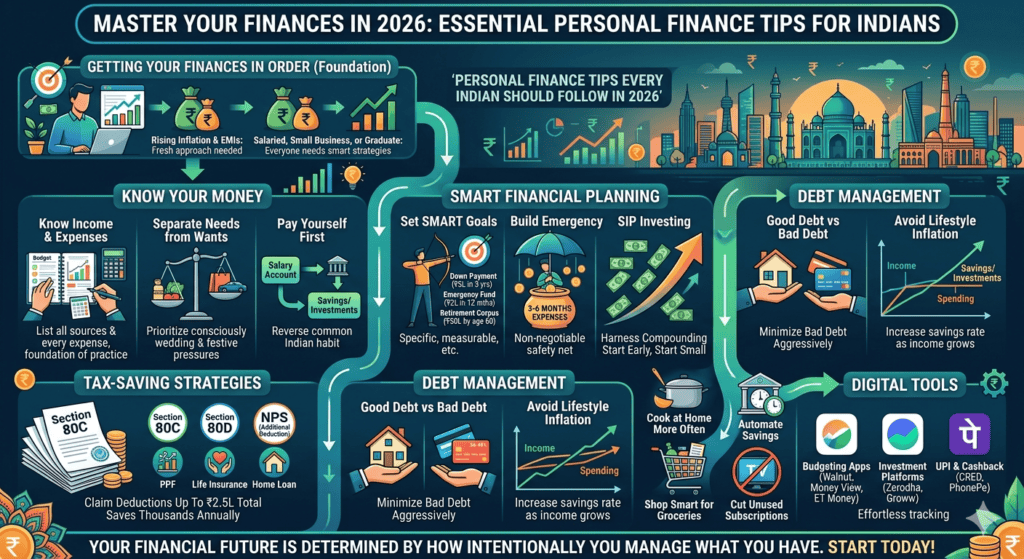

Managing money has never been more important — or more challenging — for the average Indian. Between rising inflation, fluctuating EMIs, and a fast-changing job market, getting your finances in order in 2026 demands a fresh, informed approach. Whether you are a salaried professional in Mumbai, a small business owner in Jaipur, or a young graduate just entering the workforce in Bengaluru, smart personal finance India strategies can make the difference between financial stress and genuine freedom.

This guide covers practical, actionable money management tips tailored specifically to Indian realities — from GST-era budgeting to SIP investing, Section 80C tax deductions, and digital payment habits. You will find proven methods rooted in financial planning India experts recommend, adapted for Indian households, incomes, and aspirations.

Whether you want the best way to save money, reduce unnecessary debt, or simply understand where your salary disappears every month, this blog has you covered. Let’s build your financial future, one smart step at a time.

Why Personal Finance India Matters More Than Ever in 2026

India’s economic landscape in 2026 is full of promise — and pressure. With a GDP growth rate among the highest in the world, a booming startup ecosystem, and increasing access to digital financial tools, Indians have more opportunities to grow wealth than ever before.

But here is the hard truth: most Indian households still lack a written budget, a proper emergency fund, or a clear investment plan. A large segment of working Indians live paycheck to paycheck, even as salaries rise. The cost of living in metro cities continues to climb. Home loan EMIs are heavier. Children’s education and healthcare costs are soaring.

This is exactly why understanding personal finance India concepts — and acting on them — is no longer optional. It is the single most impactful skill you can develop in 2026.

The encouraging news? You do not need to be rich to practise good personal finance India habits. You just need to be consistent, intentional, and willing to start.

Top Money Management Tips for Indians in 2026

Good money management tips are not about deprivation. They are about awareness and control. Here are the foundational principles every Indian should adopt this year.

1. Know Your Income and Expenses Inside Out

The first and most powerful of all money management tips is deceptively simple: know exactly how much money comes in and goes out every month. Sounds obvious, yet most people are genuinely surprised when they sit down and audit their spending.

List every source of income — salary, freelance work, rental income, returns on investments. Then list every expense — rent or EMI, groceries, utilities, subscriptions, dining out, fuel, clothing, and entertainment. Include irregular expenses like annual insurance premiums or festive shopping.

This 360-degree view is the foundation of sound personal finance India practice. You cannot manage what you do not measure.

2. Separate Needs from Wants

A cornerstone of all effective money management tips is distinguishing between needs (rent, food, medicine, basic utilities) and wants (branded clothing, eating out five times a week, the latest smartphone). This does not mean eliminating wants entirely — it means prioritising consciously.

In the Indian context, this distinction is especially important during wedding seasons, festive periods, and when social pressure to spend is high. Many Indians overspend on occasions to maintain appearances, often going into debt unnecessarily.

Before every significant purchase, ask: Is this a need or a want? Can I afford it without touching savings or taking a loan?

3. Pay Yourself First

One of the most effective money management tips across cultures is the “pay yourself first” principle. As soon as your salary hits your account, transfer a fixed amount directly to savings or investment accounts — before you pay bills, before you buy anything.

This reverses the common Indian habit of spending first and saving whatever remains (which is often nothing). Automating this process removes the temptation to spend and builds wealth systematically over time.

Smart Financial Planning India Strategies for 2026

Effective financial planning India style goes beyond saving. It involves setting goals, managing risk, and building multiple streams of financial security.

Set SMART Financial Goals

Every solid financial planning India framework starts with clear goals. Use the SMART framework — Specific, Measurable, Achievable, Relevant, and Time-bound — to define what you want.

Examples of SMART financial goals for Indians in 2026:

- Save ₹5 lakh for a down payment on a flat within 3 years

- Build a ₹2 lakh emergency fund within 12 months

- Accumulate ₹50 lakh in retirement corpus by age 60

- Pay off personal loan completely within 18 months

Without specific goals, financial planning India efforts remain vague and easy to abandon. With clear targets, every financial decision becomes intentional.

Build an Emergency Fund — This Is Non-Negotiable

If there is one thing that 2020 taught every Indian, it is this: emergencies happen. Job losses, medical crises, sudden home repairs — life is unpredictable.

An emergency fund is 3 to 6 months of your total monthly expenses kept in a liquid, accessible account — ideally a high-interest savings account or a liquid mutual fund. This is not an investment. It is your financial safety net.

Without an emergency fund, any unexpected expense forces you to break long-term investments, take high-interest personal loans, or borrow from family. Building this fund is step one of every financial planning India blueprint.

Start SIP Investing Early — Even with Small Amounts

Systematic Investment Plans (SIPs) are one of India’s most powerful tools for long-term wealth creation. With SIPs, you invest a fixed amount every month in a mutual fund — as little as ₹500 — and harness the power of compounding over time.

Consider this: a monthly SIP of ₹5,000 at an average annual return of 12% over 20 years grows to approximately ₹49.5 lakh. The same amount invested for 30 years becomes nearly ₹1.76 crore.

Financial planning India experts consistently emphasise that it is not the amount you invest but the habit and duration that matter most. Start small. Start today. Stay consistent.

Diversify Your Investment Portfolio

Do not put all your eggs in one basket. A balanced financial planning India portfolio typically includes:

- Equity Mutual Funds — for long-term growth (5-year horizon or more)

- Debt Funds or FDs — for stability and short-term goals

- Public Provident Fund (PPF) — for tax-free, long-term savings

- National Pension System (NPS) — for retirement planning

- Gold — as a hedge against inflation (5-10% of portfolio)

- Real Estate — if affordable, as a long-term asset

Diversification ensures that poor performance in one asset class does not devastate your entire financial plan.

Best Ways to Save Money in India — Practical 2026 Guide

Finding the best way to save money is a priority for millions of Indian households. Here are strategies that genuinely work in the Indian economic context.

Apply the 50/30/20 Rule

The 50/30/20 budgeting rule is widely considered the best way to save money for those who are new to personal finance. It works like this:

- 50% of income goes to needs (rent, EMIs, groceries, utilities)

- 30% of income goes to wants (dining, shopping, entertainment)

- 20% of income goes to savings and investments

For someone earning ₹60,000 per month, this means ₹30,000 for essentials, ₹18,000 for discretionary spending, and ₹12,000 locked away for savings and investment.

This rule is the best way to save money because it is simple, flexible, and immediately actionable. Adjust the percentages based on your income level and goals — if you have debt, divert more to repayment from the “wants” category.

Automate Your Savings and Investments

One of the most underrated ways to save money is automation. Set up standing instructions with your bank to auto-transfer a fixed amount to a recurring deposit, liquid fund, or savings account on your salary credit date.

This eliminates the willpower requirement. You never have to “decide” to save — it happens automatically, every month, without fail. This is a keystone habit in personal finance India best practices.

Cut Subscriptions and Recurring Costs You Do Not Use

Do a monthly audit of your subscriptions — OTT platforms, gym memberships, cloud storage plans, magazine subscriptions, app upgrades. Most Indians are paying for 3-5 services they barely use.

Cancelling even two unused subscriptions at ₹500 each saves ₹12,000 a year. That is the best way to save money without changing your lifestyle at all — just trimming invisible leaks.

Cook at Home More Often

Food is one of the biggest expense categories for urban Indians. Zomato and Swiggy orders add up fast — a daily order habit can easily cost ₹6,000-₹10,000 per month. Cooking at home is not just one of the best — it is also healthier.

Batch cooking on weekends, meal planning for the week, and preparing breakfast and lunch at home can save ₹3,000-₹5,000 a month for a single person and significantly more for families.

Budgeting Tips That Actually Work for Indian Households

Budgeting tips are only useful if they are actually practical for how Indian households operate. Here are methods that work in real life, not just in theory.

Use Zero-Based Budgeting for Total Control

Zero-based budgeting is one of the most powerful budgeting tips for people who want complete control over their money. In this system, every rupee of your income is assigned a specific purpose — spending, saving, or investing — until you reach zero.

If you earn ₹80,000 a month, you plan how every single rupee will be used until your “available balance” is zero. Nothing is left unaccounted for. This approach removes any ambiguity and prevents mindless spending.

Zero-based budgeting is especially effective for Indian households with variable expenses across different months.

Plan for Festive and Seasonal Expenses

Among the most India-specific budgeting tips is this: plan ahead for Diwali, weddings, and festive seasons. These are predictable, recurring events — yet most Indians overspend on them every single year and often fund them with credit cards or personal loans.

Create a “festive fund” — a dedicated savings jar or recurring deposit where you set aside ₹2,000-₹5,000 every month. By October, you will have enough to celebrate without going into debt.

This is one of the most overlooked budgeting tips in the Indian context, but one of the highest-impact ones.

Envelope Method — Digital or Physical

The envelope budgeting method is among the time-tested budgeting tips that work for all income levels. Divide your monthly budget into categories — groceries, transport, dining, shopping — and allocate a specific cash (or digital) limit to each.

In India’s increasingly UPI-driven economy, you can replicate this digitally: use different savings wallets or bank accounts for different spending categories. When one “envelope” is empty, that category is done for the month.

Track Spending Weekly, Not Monthly

Most people review their budget at month-end and find it is too late to course-correct. Among the most practical budgeting tips: do a quick 10-minute review every Sunday evening. Check which categories are on track and which are at risk.

Weekly check-ins keep you aware and in control. This habit is one of the highest-impact, lowest-effort budgeting tips available.

Practical Ways to Save Money on Daily Expenses

Beyond big-picture strategies, there are numerous ways to save money on daily expenses that compound into significant savings over the year.

Shop Smart for Groceries

Grocery shopping is one of the easiest areas to cut costs. Here are practical ways to save money at the supermarket or kirana store:

- Buy in bulk for non-perishables like pulses, rice, oil, and spices

- Shop with a list — avoid impulse buys

- Choose store brands over premium labels where quality is comparable

- Use loyalty points and credit card cashback on grocery spends

- Avoid shopping when hungry — a proven trigger for overspending

Implementing these ways to save money on groceries can reduce your monthly food bill by 15-25% without reducing quality.

Reduce Utility Bills

Utility bills are a significant monthly cost for Indian families. Simple ways to save money on electricity and water:

- Switch to LED lighting throughout the home

- Set AC temperature to 24°C — the Bureau of Energy Efficiency recommends this as the optimal balance between comfort and energy saving

- Turn off appliances at the switch, not just on standby

- Use washing machines with full loads only

- Install low-flow taps and showerheads to reduce water consumption

These ways to save money on utilities may seem small individually but often save ₹500-₹1,500 per month, adding up to ₹6,000-₹18,000 annually.

Use Public Transport and Carpooling

Fuel and vehicle maintenance are major expenses for Indian households. If your commute allows it, using metro rail, buses, or carpooling apps like Quick Ride can dramatically reduce monthly transport costs.

Even switching from daily cab rides to a monthly public transport pass is among the most effective ways to save money in urban India. For those who drive, maintaining correct tyre pressure and avoiding aggressive acceleration can improve fuel efficiency by up to 15%.

Tax-Saving Strategies: Essential Personal Finance India Knowledge

Tax planning is an inseparable part of personal finance India. Indians have access to several legitimate, government-backed deductions that can save thousands of rupees annually.

Maximise Section 80C Deductions

Under Section 80C of the Income Tax Act, you can claim deductions of up to ₹1.5 lakh per year on qualifying investments and expenses, including:

- ELSS Mutual Funds — equity-linked, with a 3-year lock-in and market-linked returns

- PPF Contributions — 15-year lock-in with tax-free, government-guaranteed returns

- EPF Contributions — automatically deducted if salaried

- Life Insurance Premiums

- Principal repayment of home loans

- Tuition fees for children

For someone in the 30% tax bracket, maxing out Section 80C alone saves ₹45,000 in taxes per year. This is non-negotiable personal finance India planning.

Use Section 80D for Health Insurance Deductions

Premiums paid for health insurance for yourself, your spouse, children, and parents qualify for deduction under Section 80D. The limit is ₹25,000 for self/family and an additional ₹25,000-₹50,000 for parents (depending on age).

Health insurance is not just a tax-saving tool — it protects your finances from catastrophic medical expenses. Both as financial protection and as a tax deduction, it is essential personal finance India practice.

Contribute to NPS for Additional Deduction

The National Pension System (NPS) offers an additional deduction of up to ₹50,000 under Section 80CCD(1B), over and above the ₹1.5 lakh 80C limit. This effectively means up to ₹2 lakh in deductions for combined 80C + NPS contributions.

NPS also builds a retirement corpus, making it one of the most effective dual-purpose tools in personal finance India — tax saving today, financial security tomorrow.

Debt Management: A Critical Part of Financial Planning India

Debt is not inherently bad — a home loan or education loan can be a stepping stone. But unmanaged debt is one of the biggest threats to personal financial health in India.

Understand Good Debt vs. Bad Debt

Good debt is used to acquire assets that appreciate or generate income — a home loan or a business loan. Bad debt is used to fund consumption — credit card balances, personal loans for holidays or gadgets.

Part of sound financial planning India is minimising bad debt aggressively. Credit card interest rates in India range from 36% to 48% annually. Even a small revolving balance can spiral quickly. Pay your full credit card bill every month — without exception.

Use the Debt Avalanche Method

If you have multiple debts, the debt avalanche method is mathematically the best approach. List all your debts by interest rate, from highest to lowest. Pay minimum dues on all, but direct every extra rupee to the highest-interest debt first.

Once the most expensive debt is cleared, move to the next. This method minimises total interest paid and is a core financial planning India strategy for debt freedom.

Avoid Lifestyle Inflation

As salaries rise, many Indians expand their lifestyle proportionally — bigger home, newer car, more expensive holidays. This is lifestyle inflation, and it is one of the most insidious traps in personal finance. Your savings rate should increase as income increases, not remain the same.

Digital Tools for Smarter Personal Finance India Management

India’s fintech ecosystem in 2026 offers incredible tools to manage your personal finance India journey more efficiently.

Budgeting Apps to Try:

- Walnut — automatically tracks spending from SMS alerts

- Money View — links to bank accounts for real-time expense tracking

- ET Money — combines mutual fund investment, insurance, and expense tracking

- Jupiter — smart savings features with spend analytics

Investment Platforms:

- Zerodha / Coin — for direct mutual funds and stocks

- Groww — beginner-friendly SIP and stock investing

- Paytm Money — seamless NPS and mutual fund investments

UPI and Cashback: Use CRED, PhonePe, or Google Pay not just for convenience but to track spending patterns and earn cashback. These tools make the “tracking” element of all good money management tips effortless.

Common Personal Finance Mistakes Indians Make

Even well-intentioned savers fall into these traps. Recognising them is the first step to avoiding them.

- No insurance before investments — Protecting what you have is more important than growing what you do not. Term life and health insurance must come before any investment.

- Trusting chit funds or unregistered schemes — Guaranteed high returns with no risk are always a red flag. Stick to SEBI-registered investment products.

- Ignoring inflation — Keeping all savings in a savings bank account that earns 3-4% while inflation runs at 5-6% means losing money in real terms every year.

- No retirement planning until it’s late — Many Indians depend on children for retirement support. This is a fragile plan. Start building your own retirement corpus from day one.

- Treating a gold loan as a savings strategy — Gold is a cultural and sentimental asset in India. Pledging it repeatedly as an emergency source is not the same as having an emergency fund.

- Mixing insurance with investment — ULIPs and endowment plans rarely deliver good returns. Buy term insurance for protection and mutual funds for growth — separately.

Conclusion

Mastering personal finance India habits is not about perfection — it is about progress. Every rupee you save, every debt you reduce, and every investment you make compounds over time into financial freedom and security.

The money management tips and financial planning India strategies in this guide are not theoretical — they are practical, proven, and designed for real Indian life. Whether you are starting from zero or looking to level up an existing plan, the principles remain the same: know your money, give it purpose, protect it wisely, and grow it patiently.

Commit to at least three saving money tips from this guide this month. Set up a SIP. Cancel one unused subscription. Start your emergency fund. Review your tax deductions. These small actions, taken consistently, are the best way to save money and build wealth in 2026.

Your financial future is not determined by how much you earn — it is determined by how intentionally you manage what you have. Start today.

Frequently Asked Questions

Q1: What is the best way to start with personal finance in India if I have no savings?

Start by tracking your expenses for one month to understand where your money goes. Then open a separate savings account and transfer even ₹1,000 on your salary date. This begins the habit. Simultaneously, get a basic health insurance policy if you do not have employer coverage. These two steps — tracking and insuring — are the foundation of personal finance India practice for beginners.

Q2: How much of my salary should I save every month?

Financial planning India experts generally recommend saving at least 20% of your take-home salary. If that is not immediately possible, start with 10% and increase by 1-2% every six months. The percentage matters less than the consistency. Even ₹2,000 a month invested in a SIP for 25 years at 12% returns grows to over ₹37 lakh.

Q3: What are the best budgeting tips for Indian families with irregular income?

If your income is variable — you are a freelancer, consultant, or business owner — base your budget on your lowest expected monthly income. Save and invest from surplus months into a buffer fund. This way, lean months do not derail your financial plan. Among budgeting tips for irregular income earners, this is the most important.

Q4: Are credit cards good or bad for personal finance in India?

Credit cards are powerful tools when used correctly. They offer rewards, cashback, fraud protection, and help build a credit score. They become dangerous only when you carry a balance. The golden rule: never spend on credit what you cannot pay in full that month. Used this way, credit cards are an asset, not a liability.

Q5: What are the best saving money tips for young Indians just starting their careers?

Three essential saving money tips for young professionals: (1) Start a SIP immediately, even with ₹500. Time is your greatest asset. (2) Live below your means in your 20s — resist peer pressure to upgrade your lifestyle too quickly. (3) Build an emergency fund of at least 3 months’ expenses before investing aggressively. These saving money tips in early career set the foundation for lifelong financial health.

Q6: How can I save money on taxes legally in India?

Maximise Section 80C investments (₹1.5 lakh), contribute to NPS for an additional ₹50,000 deduction, buy health insurance for Section 80D benefits, and if you have a home loan, claim both principal (80C) and interest (Section 24) deductions. These are all legitimate, government-endorsed financial planning India strategies.