Introduction

Managing your money wisely is one of the smartest decisions you can make for your future. Yet, most Indians struggle with where to start. Whether you want to grow your savings, plan for retirement, or build long-term wealth, finding the right financial advisor in India can make all the difference.

The Indian financial landscape is evolving rapidly. With thousands of investment options — mutual funds, stocks, real estate, gold, and government schemes — it’s easy to feel overwhelmed. That’s where a qualified personal financial advisor in India steps in. They cut through the noise, understand your goals, and design a roadmap built just for you.

In this guide, we cover everything you need to know — from how to choose the best financial advisor in India, to money management tips, saving money tips, and budget planning in India that can transform your financial future.

Why You Need a Financial Advisor in India

Most people believe financial advisors are only for the wealthy. That’s a myth.

A skilled financial advisor online India can help someone earning ₹30,000 per month just as effectively as a high-net-worth individual. Here’s why hiring an advisor is a game-changer:

- Goal Clarity: An advisor helps you define short-term and long-term financial goals.

- Tax Planning: Save more by using legal tax-saving instruments smartly.

- Risk Management: Protect your wealth with the right insurance and diversified portfolio.

- Disciplined Investing: Avoid emotional decisions during market volatility.

- Retirement Security: Build a retirement corpus that sustains your lifestyle.

Without a plan, most people either under-invest or make costly mistakes. A personal finance India expert gives you the framework to grow wealth systematically.

Top 10 Financial Advisor in India — What to Look For

Before we dive into names, it’s important to understand what makes someone among the top 10 financial advisors in India. Not every advisor is equal. Here’s what separates the best from the rest:

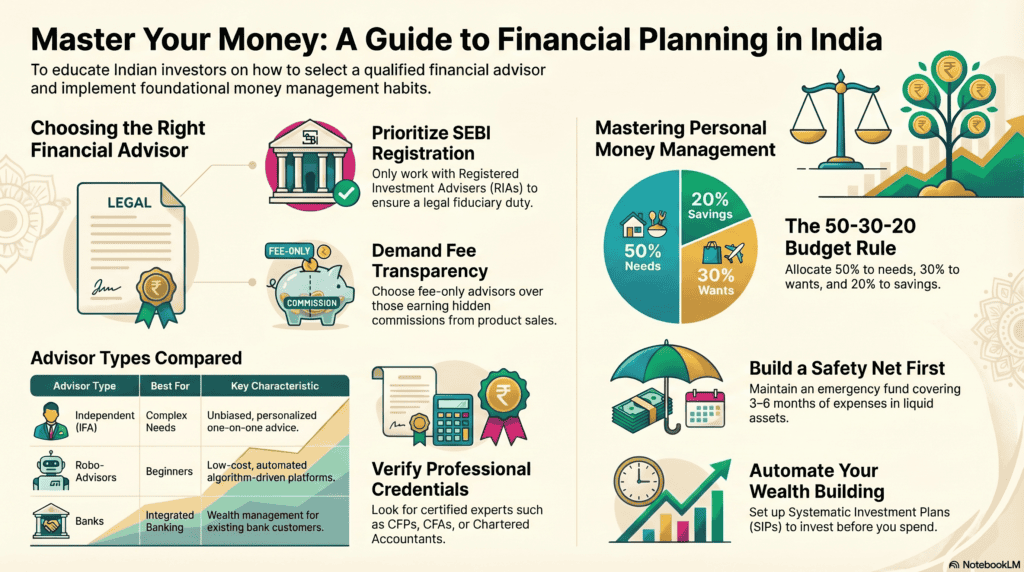

1. SEBI Registration

Always check if the advisor is registered with the Securities and Exchange Board of India (SEBI) as a Registered Investment Adviser (RIA). This ensures they are legally qualified and bound by fiduciary duty — meaning they must act in your best interest, not theirs.

2. Fee Transparency

The best financial consultants in India are transparent about their fees. Avoid advisors who earn hidden commissions from selling you products. Look for fee-only advisors who charge a flat fee or percentage of assets managed.

3. Track Record and Credentials

Look for certifications like CFP (Certified Financial Planner), CFA (Chartered Financial Analyst), or CA (Chartered Accountant). These credentials signal deep expertise in personal finance India matters.

4. Personalized Approach

Your financial situation is unique. The best advisors don’t offer cookie-cutter plans. They take time to understand your income, liabilities, risk appetite, family goals, and future aspirations before crafting a strategy.

5. Technology Integration

Leading best online financial advisor India platforms now use AI-driven tools, goal-tracking dashboards, and real-time portfolio monitoring. This makes it easier for you to stay on top of your finances anytime, anywhere.

Best Financial Advisor in India — Categories to Know

India has a diverse ecosystem of financial advisory services. Here’s a breakdown of the main types:

Independent Financial Advisors (IFAs)

These are individual SEBI-registered advisors who offer unbiased advice. Since they aren’t tied to any product company, they’re more likely to recommend what truly suits you.

Best for: Personalized one-on-one advice, high-net-worth individuals, complex financial situations.

Robo-Advisors and Best Online Financial Advisor India Platforms

Digital platforms like Zerodha Coin, Groww, ET Money, and Scripbox offer algorithm-driven investment advice at low costs. These are ideal if you’re comfortable managing money online and prefer automation.

Best for: First-time investors, millennials, those seeking low-cost solutions.

Banks and NBFCs

Wealth management divisions of major banks (SBI, HDFC, ICICI, Axis) offer financial planning services, though advisors here may push in-house products.

Best for: Existing bank customers looking for integrated wealth management.

Certified Financial Planners (CFPs)

CFPs in India undergo rigorous training and examinations. Finding a CFP among the best financial consultants in India ensures you’re working with a credentialed professional who follows ethical standards.

Best for: Comprehensive financial planning — retirement, tax, estate, and insurance.

Best Personal Finance Websites India — Tools to Help You Plan

Even before hiring an advisor, you can take charge of your personal finance India journey using these trusted online resources:

- Moneycontrol: Real-time market data, portfolio tracking, and personal finance articles.

- ET Money: Mutual fund investing, expense tracking, and insurance comparison in one app.

- Paisabazaar: Compare loans, credit cards, and insurance products side by side.

- Groww: Simplified stock and mutual fund investing for beginners.

- NPS Trust Portal: Manage your National Pension System account directly.

- Scripbox: Goal-based mutual fund investing with guided recommendations.

These platforms are among the best personal finance websites India has to offer. They help you learn, plan, and invest — often for free.

Money Management Tips Every Indian Should Follow

Before you even consult a financial advisor in India, building strong money habits is essential. Here are proven money management tips that work:

Track Every Rupee

The first rule of personal finance is awareness. Use apps like ET Money or a simple spreadsheet to record every income and expense. You can’t manage what you don’t measure.

Pay Yourself First

Before spending, set aside at least 20% of your monthly income for investments and savings. Automate SIPs (Systematic Investment Plans) so this happens without willpower.

Avoid Lifestyle Inflation

Every time your salary increases, resist the urge to proportionally increase spending. Channel that extra income into investments instead.

Build an Emergency Fund

Keep 3–6 months of monthly expenses in a liquid instrument (savings account or liquid mutual fund). This protects you from financial shocks without derailing your investment plan.

Review Your Finances Quarterly

Markets change. Life changes. Review your portfolio and financial plan every three months with your personal financial advisor India to stay on track.

Saving Money Tips That Actually Work in India

Saving isn’t about being frugal — it’s about being intentional. Here are practical saving money tips tailored for Indian households:

Use the 50-30-20 Rule

Divide your monthly take-home income as follows:

- 50% for needs (rent, groceries, utilities, EMIs)

- 30% for wants (dining, shopping, entertainment)

- 20% for savings and investments

This simple framework is one of the most effective tools in personal finance India.

Leverage Tax-Saving Investments

India offers generous tax deductions under Section 80C (up to ₹1.5 lakh), 80D (health insurance), and NPS contributions. Maximizing these not only saves tax but also builds wealth.

Cut Subscription Clutter

Review all recurring subscriptions monthly. Cancel unused OTT platforms, magazine subscriptions, or gym memberships. These small savings add up significantly over a year.

Buy Term Insurance Early

A pure term insurance plan at age 25–30 costs a fraction of what it does at 40. Buying early is one of the smartest saving money tips for long-term financial security.

Prepay Loans Strategically

Home loans and personal loans carry high interest burdens. Whenever you have surplus funds, make partial prepayments to reduce interest outgo. Always check for prepayment penalties first.

Budget Planning India — A Step-by-Step Framework

Effective budget planning India is the cornerstone of financial freedom. Here’s a simple, actionable framework:

Step 1: Calculate Your Monthly Net Income

Start with your in-hand salary after all deductions — PF, TDS, professional tax. Include all income sources: salary, freelance, rental income, etc.

Step 2: List All Fixed Expenses

Fixed expenses don’t change month to month. These include:

- House rent or home loan EMI

- Car loan EMI

- Insurance premiums

- School fees

Step 3: Estimate Variable Expenses

Variable expenses fluctuate. Estimate these based on last 3 months:

- Groceries and household supplies

- Utility bills

- Transportation

- Dining out and entertainment

Step 4: Allocate for Savings and Investments

After accounting for fixed and variable expenses, allocate what remains (or what you’ve committed) toward:

- SIPs in mutual funds

- PPF or NPS contributions

- Emergency fund top-up

- Short-term savings goals

Step 5: Identify Gaps and Plug Them

If your expenses exceed income, you have a deficit. Work with a financial advisor in India to identify where cuts can be made or how income can be supplemented.

Step 6: Automate and Stick to the Plan

Set up automatic transfers for investments and savings on salary day. The less manual intervention required, the more consistent your budget will be.

How to Choose the Best Financial Advisor in India for Your Needs

Here’s a practical checklist when shortlisting the best financial advisor in India:

Verify SEBI RIA Registration Ask for their SEBI registration number and verify it on the SEBI website.

Understand Their Fee Model Are they fee-only, commission-based, or a hybrid? Fee-only advisors tend to have fewer conflicts of interest.

Ask About Their Planning Process A good advisor will ask you many questions before recommending anything. If they immediately try to sell you a product, walk away.

Request Client References Credible advisors are happy to share testimonials or put you in touch with existing clients.

Assess Communication Style Financial planning is a long relationship. Choose someone you’re comfortable talking to, who explains complex terms simply.

Check Specialization Some advisors specialize in retirement planning, others in tax, NRI planning, or business finance. Match their expertise to your primary need.

Financial Advisor Online India — Is Digital Advisory Right for You?

The rise of financial advisor online India platforms has democratized wealth management. No longer do you need to be in a metro city to access quality advice.

Online advisors offer:

- Lower costs compared to traditional wealth managers

- 24/7 dashboard access to monitor your portfolio

- Automated rebalancing to keep your asset allocation on track

- Goal-based planning tools for home buying, education, retirement

- Video consultations with qualified CFPs and advisors

However, online platforms work best for those with relatively straightforward financial situations. If you have complex needs — business income, multiple properties, estate planning, or NRI tax implications — a dedicated personal financial advisor India may serve you better.

Conclusion

Your financial future is too important to leave to chance. Whether you’re just starting your career, planning for your child’s education, or approaching retirement, partnering with the best financial advisor in India gives you a proven edge.

From smart money management tips and disciplined saving money tips to structured budget planning India strategies, a good advisor helps you convert your income into lasting wealth. The Indian financial ecosystem today — with its blend of SEBI-registered advisors, digital platforms, and certified planners — gives every individual access to quality financial guidance.

Take the first step today. Research the top 10 financial advisor in India, ask the right questions, and choose a partner who aligns with your goals and values. Your future self will thank you.

Frequently Asked Questions

What does a financial advisor in India charge?

Fees vary widely. SEBI-registered RIAs typically charge ₹5,000–₹50,000 per year for a comprehensive financial plan, or 0.5%–1% of assets under advisory. Online platforms may charge as little as ₹500–₹2,000 per month.

Is it safe to use an online financial advisor in India?

Yes, provided the platform or advisor is SEBI-registered. Always verify credentials before sharing personal or financial information.

How is a financial advisor different from a mutual fund distributor?

A mutual fund distributor earns commissions from selling funds and is not required to act in your best interest. A SEBI-registered investment adviser is a fiduciary — legally obligated to prioritize your interests.

At what age should I start working with a financial advisor?

The earlier, the better. Starting in your 20s gives your investments maximum time to compound. However, it’s never too late — even starting at 40 or 50 can dramatically improve your retirement readiness.

Can a financial advisor help with tax planning in India?

Yes. Most qualified financial advisors work in conjunction with tax consultants or are themselves qualified to advise on tax-saving investments, deductions, and efficient income structuring.

What is the difference between personal finance and wealth management?

Personal finance covers everyday money management — budgeting, saving, insurance, and basic investing. Wealth management is a broader, more sophisticated service for high-net-worth individuals, covering estate planning, succession, and complex investment strategies.