Smart Tax-Saving Strategies in India Maximize savings with India’s latest income tax law. Explore ELSS, PPF, NPS, health insurance, home loan benefits, and regime comparison. with Latest Income Tax Law

Why Tax Planning Matters More Than Ever

Tax planning isn’t just about reducing liability—it’s about building wealth, protecting your family, and aligning with India’s evolving financial laws. With the latest income tax law for FY 2025–26, taxpayers face a crucial choice: stick with the old regime full of deductions or embrace the new regime with lower slab rates and simplicity.

🧾 Best Tax-Saving Options Under Old Regime

The old regime remains attractive for those with higher deductions.

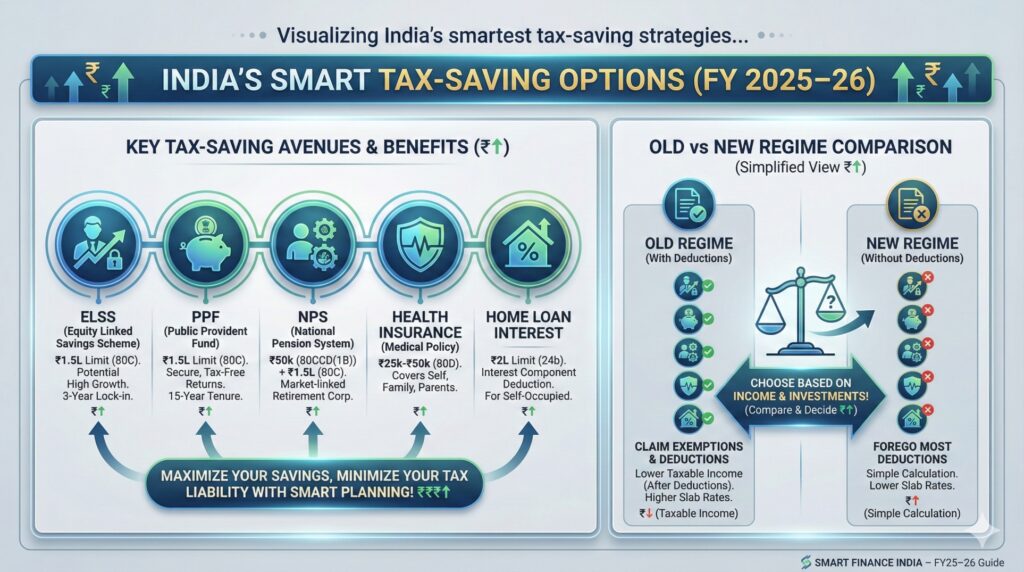

🔹 Section 80C (₹1.5 lakh limit)

- ELSS Mutual Funds: 3-year lock-in, potential double-digit returns, tax-efficient.

- PPF (Public Provident Fund): Safe, 15-year maturity, tax-free interest (~7.1%).

- NPS (National Pension System): Extra ₹50,000 deduction under 80CCD(1B).

- Sukanya Samriddhi Yojana: For girl child, ~8.2% interest, tax-free.

- Tax-Saving FDs: 5-year lock-in, interest taxable.

🔹 Section 80D: Health Insurance

- ₹25,000 deduction for self/family.

- ₹50,000 for senior citizen parents.

🔹 Section 24(b): Home Loan Interest

- Deduction up to ₹2 lakh for self-occupied property.

🔹 Section 80E: Education Loan Interest

- No cap, valid for 8 years.

💡 Best Tax-Saving Options Under New Regime (FY 2025–26)

The new regime is now the default choice unless you opt for the old regime. It offers lower slab rates but limited deductions. Although the new regime restricts traditional deductions (like 80C, 80D), taxpayers can still save via:

- Standard Deduction (₹75,000) – Automatically available to salaried taxpayers.

- Employer’s Contribution to NPS (Sec 80CCD(2)) – Deduction for employer’s share, not capped by 80C.

- Home Loan Interest (Sec 24) – Deduction for interest on let-out property continues under the new regime.

- Relaxed Slabs – Even without deductions, lower rates + rebate up to ₹12 lakh reduce liability.

- LTCG Exemption – Equity long-term capital gains up to ₹1 lakh/year remain tax-free.

📊 Latest Income Tax Law Updates (FY 2025–26)

India’s Income Tax Law FY 2025–26 introduces higher rebates, simplified compliance, and a default new regime with zero tax up to ₹12 lakh

Policy Highlights – Finance Act 2025

- New regime is default: Taxpayers must opt-in for the old regime if they want to claim deductions.

- Zero tax up to ₹12 lakh: Thanks to enhanced Section 87A rebate (₹60,000) for incomes up to ₹12 lakh.

- Standard deduction raised to ₹75,000: Applies to salaried individuals and pensioners.

- Simplified slabs: Lower rates across brackets encourage compliance and reduce litigation.

- Terminology change: “Tax Year” replaces “Assessment Year” for clarity.

- Presumptive taxation limits expanded: Higher thresholds for small businesses and professionals.

- Digital tax rationalization: Equalisation levy on digital ads removed.

- Restructured Act: Reduced from 819 to 536 sections for simplicity.

Tip: If you have significant deductions (80C, 80D, home loan), the old regime may save more. Otherwise, the new regime offers simplicity and lower rates.

🎯 Conclusion: Choose Wisely, Save Smartly

The best tax-saving option depends on your lifestyle and financial goals.

- ELSS + PPF for balanced growth.

- NPS for retirement planning.

- Health insurance for protection + tax benefit.

- Home loan interest for wealth creation.

⚖️ Old vs New Regime: Quick Comparison

| Feature | Old Regime | New Regime (Default) |

|---|---|---|

| Tax-free income threshold | ₹2.5 lakh | ₹12 lakh |

| Deductions allowed | Yes (e.g., 80C, 80D, HRA) | No (except standard deduction) |

| Section 87A rebate | ₹12,500 | ₹60,000 |

| Standard deduction | ₹75,000 | ₹75,000 |

| Best for | High deductions/investments | Simplified filing, low deductions |

👉 The smartest move is to compare regimes early in the year and align investments with your long-term financial strategy.

❓ FAQ (Smart Tax-Saving Strategies

Q1: Which regime is better for tax saving?

Old regime suits those with high deductions; new regime benefits those with fewer exemptions.

Q2: What is the Section 80C limit?

₹1.5 lakh per year.

Q3: Can I claim health insurance under new regime?

Yes, Section 80D deductions are allowed.

Q4: What is the rebate limit under new law?

No tax up to ₹7 lakh taxable income under Section 87A.

✅ Takeaway: If you have high investments in ELSS, PPF, insurance, or housing, the old regime may still be better. But for most salaried taxpayers with fewer deductions, the new regime’s zero tax up to ₹12 lakh + simplified slabs is the smarter choice.