What Are Tax Saving Investments in India?

Every year, millions of Indian taxpayers look for the most reliable tax saving investments in India to legally reduce their income tax liability. Whether you are a salaried professional, a self-employed individual, or a business owner, understanding your options is the single most powerful step toward keeping more of your hard-earned money.

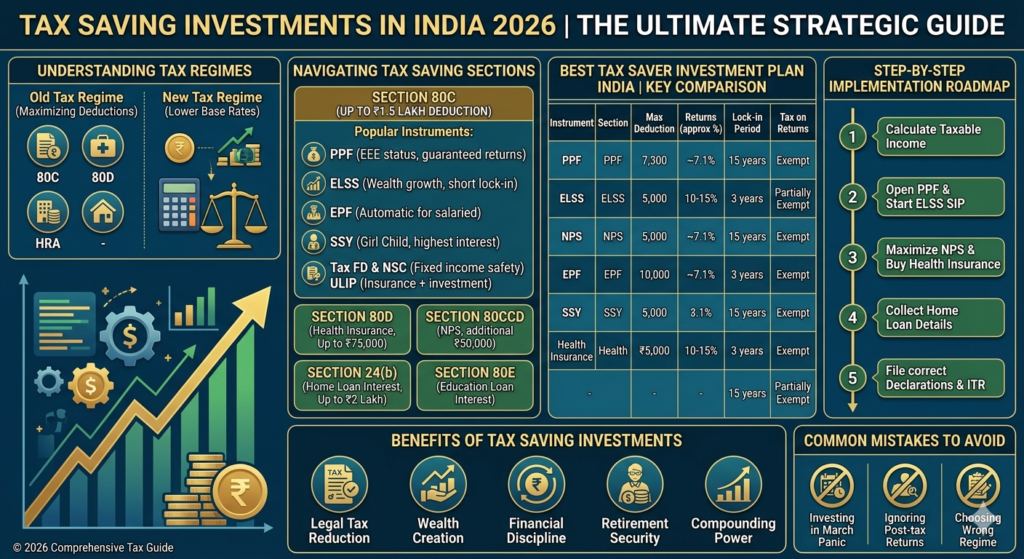

Tax saving investments in India are financial instruments and schemes approved under the Income Tax Act, 1961, that allow you to claim deductions on your taxable income. The most popular gateway is Section 80C, which permits a deduction of up to ₹1.5 lakh per financial year. Beyond 80C, there are several other sections — 80D, 80CCD, 24(b), and more — that open up additional avenues to reduce your tax burden.

In 2026, with revised tax slabs under the New Tax Regime and continued incentives under the Old Tax Regime, choosing the right tax saving investments in India matters more than ever. This comprehensive guide walks you through every option, step-by-step strategies, and the key benefits so you can make an informed decision before the financial year ends.

Best Tax Saving Investments in India 2026

India offers a wide array of tax saving investments in India suited for different risk profiles and financial goals. Here is a detailed overview of the most effective options available in 2026.

1. Public Provident Fund (PPF)

The PPF remains one of the most trusted tax free investments in the country. It falls under the EEE (Exempt-Exempt-Exempt) category, meaning your investment, interest earned, and maturity proceeds are all completely tax-free.

- Lock-in period: 15 years

- Interest rate (2026): ~7.1% per annum (subject to quarterly revision)

- Investment limit: ₹500 to ₹1.5 lakh per year

- Deduction: Under Section 80C

PPF is ideal for risk-averse investors who want guaranteed, long-term returns along with full tax exemption.

2. Equity Linked Savings Scheme (ELSS)

ELSS mutual funds are the fastest-growing category of tax saving investments in India among younger investors. They invest primarily in equities and come with a mandatory 3-year lock-in — the shortest among all 80C instruments.

- Lock-in period: 3 years

- Expected returns: 10–15% p.a. (market-linked)

- Deduction: Under Section 80C (up to ₹1.5 lakh)

- Tax on returns: LTCG over ₹1.25 lakh taxed at 12.5%

ELSS funds are the go-to choice for investors who want both tax savings and wealth creation over the medium to long term.

3. National Pension System (NPS)

The NPS is one of the best tax saving investments in India for salaried individuals who want to build a retirement corpus while saving taxes across multiple sections.

- Deduction: ₹1.5 lakh under Section 80CCD(1) + additional ₹50,000 under 80CCD(1B)

- Total possible deduction: ₹2 lakh

- Returns: Market-linked (equity + debt mix)

- Lock-in: Until age 60

NPS offers the highest combined deduction limit, making it a top-ranked best tax saver investment plan india for disciplined long-term savers.

4. Employee Provident Fund (EPF)

For salaried employees, EPF contributions are automatically one of the most effective ways to save tax in India. Your monthly contribution (12% of basic + DA) qualifies for deduction under Section 80C.

- Interest rate (2026): ~8.15% p.a.

- Tax treatment: EEE category (fully tax-free)

- Deduction: Under Section 80C

Employer contributions up to 12% are also tax-exempt, making EPF a powerful dual benefit tool.

5. Sukanya Samriddhi Yojana (SSY)

If you have a girl child, SSY is one of the finest tax saving schemes in India you can invest in. Falling under EEE status, it offers one of the highest guaranteed returns among small savings schemes.

- Interest rate (2026): ~8.2% p.a.

- Lock-in: Until the girl turns 21

- Deduction: Under Section 80C

- Eligibility: Girls below age 10

6. Tax-Saving Fixed Deposits (FD)

Tax-saving FDs from banks and post offices are among the simplest tax saving options in India for conservative investors.

- Lock-in: 5 years (no premature withdrawal)

- Interest rate: 6.5–7.5% p.a.

- Deduction: Under Section 80C

- Note: Interest earned is taxable as per your slab

They are straightforward but remember that interest income is not tax-free.

7. National Savings Certificate (NSC)

NSC is a government-backed fixed income instrument offered by post offices and is one of the popular tax saving investments in India for those who prefer capital safety.

- Interest rate (2026): ~7.7% p.a.

- Lock-in: 5 years

- Deduction: Under Section 80C

- Interest: Taxable but annual accrual qualifies as reinvestment under 80C

8. Unit Linked Insurance Plans (ULIPs)

ULIPs combine life insurance with investment and qualify as tax saving investments in India under Section 80C. Post-2021 budget changes, ULIPs with annual premium above ₹2.5 lakh are taxed on maturity.

- Lock-in: 5 years

- Deduction: Up to ₹1.5 lakh under 80C

- Returns: Market-linked

Tax Free Investments You Should Know About

Not all tax saving investments in India are tax-free on returns. Here are the true tax free investments where your money grows without any tax implication at any stage.

| Investment | Tax on Investment | Tax on Returns | Tax on Maturity |

| PPF | Deductible | Exempt | Exempt |

| EPF | Deductible | Exempt | Exempt (conditions apply) |

| SSY | Deductible | Exempt | Exempt |

| Life Insurance Maturity | Deductible | Exempt | Exempt (conditions) |

| ELSS (within ₹1.25L LTCG) | Deductible | Partially Exempt | Partially Exempt |

Choosing genuine tax free investments ensures you do not face a surprise tax bill at the time of withdrawal, which is a common mistake many investors make when planning tax saving india strategies.

Top Tax Saving Schemes in India 2026

Beyond Section 80C, there are powerful tax saving schemes in India under other sections of the Income Tax Act.

Section 80D — Health Insurance Premiums

- Deduction up to ₹25,000 for self/family

- Additional ₹25,000 for parents (₹50,000 if parents are senior citizens)

- Total possible: Up to ₹75,000 deduction

Health insurance is one of the most overlooked tax saving options in India that also provides genuine financial protection.

Section 24(b) — Home Loan Interest

- Deduction up to ₹2 lakh on interest paid for a self-occupied property

- No limit for let-out property (subject to overall set-off rules)

If you have a home loan, this is among the most significant ways to save tax in India available to you.

Section 80E — Education Loan Interest

- Full deduction on interest paid for higher education loans

- Available for 8 years from the year of first repayment

Section 80G — Donations to Charitable Organizations

- Deductions ranging from 50% to 100% of donated amount

- Only for donations made to registered charities

Section 80TTA / 80TTB — Savings Account Interest

- ₹10,000 deduction on savings account interest (non-senior citizens)

- ₹50,000 for senior citizens (80TTB — includes FD interest)

How to Choose Tax Saving Investments in India

Selecting the right tax saving investments in India depends on your financial situation, tax slab, risk appetite, and investment horizon. Here is a structured approach to help you decide.

Step 1: Identify Your Tax Regime

In 2026, taxpayers in India can choose between:

- Old Tax Regime: Allows deductions and exemptions (80C, 80D, HRA, etc.)

- New Tax Regime: Lower base tax rates but limited deductions

If you opt for the New Tax Regime, most Section 80C deductions are unavailable. Only NPS employer contribution deduction (80CCD(2)) remains applicable. So the first step is determining which regime benefits you more.

Step 2: Calculate Your Remaining Deduction Gap

Before choosing tax saving investments in India, calculate:

- What deductions you already have (EPF, home loan, school fees)

- Remaining 80C limit (₹1.5 lakh – existing deductions)

This tells you exactly how much more you need to invest in additional tax saving options in india to fully exhaust your deduction limits.

Step 3: Match Investments to Your Goals

| If Your Goal Is… | Best Tax Saving Option |

| Wealth creation + tax saving | ELSS Funds |

| Risk-free guaranteed returns | PPF, NSC, Tax-saving FD |

| Retirement planning | NPS |

| Girl child future | Sukanya Samriddhi Yojana |

| Health protection | Health Insurance (80D) |

| Home loan benefit | Interest deduction u/s 24(b) |

Step 4: Consider Lock-in Periods

Every tax saving scheme in India under 80C comes with a mandatory lock-in. Ensure you are not locking up funds you may need in the short term.

- ELSS — 3 years (shortest)

- Tax-saving FD, NSC — 5 years

- PPF — 15 years

- NPS — Until age 60

Step 5: Diversify Across Multiple Instruments

Do not put all your money into one option. A well-balanced best investment plan for tax benefit in india typically combines ELSS for growth, PPF for stability, and NPS for retirement, while using health insurance to tap into Section 80D.

Step-by-Step Guide to Start Tax Saving in India

Here is a practical, step-by-step roadmap to implement your tax saving investments in India plan starting today.

Step 1: Gather Your Financial Documents

Collect your salary slips, Form 16, existing EPF statement, insurance policy details, and home loan certificate. This gives you a clear picture of deductions already accounted for.

Step 2: Open a PPF Account (if not already)

Visit your bank branch or use net banking to open a PPF account. You can start with as little as ₹500. PPF is the foundation of any solid tax saving india strategy.

Step 3: Invest in ELSS via SIP

Select a well-rated ELSS fund and start a Systematic Investment Plan (SIP). This approach to tax saving investments in India spreads your investment over 12 months, reducing market timing risk.

Step 4: Maximize NPS Contribution

If you are salaried, request your employer to include NPS under your salary structure to claim the additional ₹50,000 deduction under Section 80CCD(1B) — one of the most underutilized tax saving options in india.

Step 5: Buy a Health Insurance Policy

Purchase a comprehensive family floater health insurance plan. This adds ₹25,000–₹75,000 in deductions under Section 80D, and is one of the smartest ways to save tax in india that also provides essential coverage.

Step 6: Check Your Home Loan Statement

If you have a housing loan, collect the annual interest certificate from your lender. Claim up to ₹2 lakh under Section 24(b) — this single deduction can significantly reduce your tax saving india liability.

Step 7: File Correct Investment Declarations with Your Employer

Submit Form 12BB to your employer before January with all your investment proofs. This ensures correct TDS deduction and avoids a large tax payment at year-end.

Step 8: File Your ITR with All Deductions

When filing your Income Tax Return, ensure all your tax saving investments in India are properly declared. Use ITR-1 or ITR-2 depending on your income sources.

Benefits of Tax Saving Investments in India

Understanding the benefits makes it easier to stay committed to your tax saving investments in India plan year after year.

1. Legal Reduction in Tax Outgo

The primary and most obvious benefit is a legal reduction in your income tax liability. Maximizing 80C + 80D + NPS can save a person in the 30% tax bracket up to ₹78,000 or more annually.

2. Wealth Creation Over Time

The best part about tax saving investments in India is that they are not just tax tools — they are also wealth creation vehicles. ELSS and NPS, in particular, generate significant long-term returns, especially when started early.

3. Financial Discipline

Committing to annual tax saving investments in India builds a habit of regular saving and investing. Over 10–20 years, this disciplined approach can create a substantial corpus.

4. Retirement Security

Instruments like PPF, EPF, and NPS — all key tax saving schemes in India — are specifically designed to build a retirement fund. They ensure you have a financially secure future beyond your earning years.

5. Protection Against Risks

Options like health insurance (Section 80D) and life insurance (Section 80C) are tax saving options in india that simultaneously protect you and your family against life’s uncertainties.

6. Power of Compounding

Long-term tax free investments like PPF and SSY benefit immensely from compounding. The interest earned is reinvested and compounds annually, making your corpus grow exponentially over time.

7. Encouragement of Social Goals

Instruments like SSY encourage savings for the girl child’s education and marriage. NSC and PPF promote a culture of long-term, disciplined saving across India’s population.

8. Diversification of Portfolio

A well-planned best tax saver investment plan india inherently diversifies your portfolio across debt (PPF, NSC), equity (ELSS), and hybrid (NPS) instruments, balancing risk and return effectively.

Best Investment Plan for Tax Benefit in India — Comparison Table

| Instrument | Section | Max Deduction | Returns | Risk | Lock-in | Tax on Returns |

| PPF | 80C | ₹1.5 lakh | 7.1% | Nil | 15 yrs | Exempt |

| ELSS | 80C | ₹1.5 lakh | 10–15% | High | 3 yrs | LTCG (12.5% above ₹1.25L) |

| NPS | 80CCD | ₹2 lakh | 8–12% | Medium | Age 60 | Partial |

| EPF | 80C | ₹1.5 lakh | 8.15% | Nil | Service period | Exempt |

| SSY | 80C | ₹1.5 lakh | 8.2% | Nil | 21 yrs | Exempt |

| Tax FD | 80C | ₹1.5 lakh | 6.5–7.5% | Nil | 5 yrs | Taxable |

| NSC | 80C | ₹1.5 lakh | 7.7% | Nil | 5 yrs | Taxable |

| Health Insurance | 80D | ₹75,000 | N/A | Nil | Annual | N/A |

This comparison table serves as a quick reference when determining the best investment plan for tax benefit in india suited to your profile.

Common Mistakes to Avoid in Tax Saving India

Even informed investors make errors when planning tax saving investments in India. Avoid these pitfalls.

1. Investing in March Panic Waiting until the last minute (February–March) to invest in tax saving investments in India forces you into lump-sum investments and poor decision-making. Start in April (beginning of financial year) via SIPs.

2. Ignoring Returns While Chasing Deductions Many investors choose tax-saving FDs or insurance-linked products only for the deduction, ignoring that post-tax returns may be lower than other tax saving options in india.

3. Not Using Section 80D A large section of taxpayers leave Section 80D money on the table. Health insurance premiums are among the easiest and most impactful ways to save tax in india.

4. Overlooking NPS 80CCD(1B) The additional ₹50,000 NPS deduction over and above 80C is consistently underutilized. It is one of the finest tax saving options in india available to salaried individuals.

5. Choosing Wrong Tax Regime In 2026, not evaluating whether the Old or New Tax Regime works better for you can cost you significantly. Always run a comparison before the financial year begins.

6. Mixing Insurance with Investment Traditional insurance-cum-investment plans often offer poor returns and sub-optimal insurance cover. Keep your insurance and tax saving investments in india separate for better outcomes.

Conclusion

Planning your tax saving investments in India is not just a compliance exercise — it is a powerful strategy to build long-term wealth while legally minimizing your tax burden. In 2026, with both the Old and New Tax Regimes available, a personalized approach is essential.

Start early in the financial year, diversify across instruments like PPF, ELSS, NPS, and health insurance, and always align your tax saving investments in India with your broader financial goals. Whether you seek the security of tax free investments like PPF and SSY or the growth potential of ELSS, the right combination can save you lakhs in taxes and simultaneously build a robust financial foundation.

Take the first step today — calculate your taxable income, identify your deduction gap, and invest in the best tax saver investment plan india that fits your life stage and goals. Your future self will thank you for it.

Frequently Asked Questions

Q1. What are the best tax saving investments in India for 2026?

The best tax saving investments in India in 2026 include PPF (EEE category, 7.1% returns), ELSS mutual funds (highest return potential, 3-year lock-in), NPS (₹2 lakh combined deduction), Sukanya Samriddhi Yojana (8.2% for girl child), and health insurance under Section 80D. The ideal mix depends on your income, tax slab, and risk appetite.

Q2. Which are truly tax free investments in India?

Truly tax free investments in India where all three stages — contribution, interest, and maturity — are exempt include PPF, EPF (subject to conditions), Sukanya Samriddhi Yojana, and maturity proceeds of life insurance policies (subject to premium-to-sum assured ratio rules). ELSS returns up to ₹1.25 lakh LTCG annually are also tax-free.

Q3. Can I claim more than ₹1.5 lakh in tax saving investments in India?

Yes. While Section 80C has a ₹1.5 lakh cap, you can claim additional deductions through Section 80CCD(1B) (₹50,000 for NPS), Section 80D (up to ₹75,000 for health insurance), and Section 24(b) (up to ₹2 lakh for home loan interest). So your total deductions from tax saving investments in India can exceed ₹5 lakh in some cases.

Q4. What are the best tax saving options in India for salaried employees?

For salaried individuals, the best tax saving options in india are EPF (auto-deducted, fully exempt), ELSS mutual funds (highest growth), NPS (extra ₹50,000 deduction), and health insurance under 80D. Adding a home loan interest deduction under Section 24(b) further boosts tax savings.

Q5. How do tax saving schemes in India work under the new tax regime?

Under the New Tax Regime (2026), most tax saving schemes in India under Section 80C, 80D, and HRA are not available. The only notable exceptions are the employer’s NPS contribution (80CCD(2)) and the standard deduction of ₹75,000 for salaried individuals. If you have significant deductions, the Old Tax Regime may still be more beneficial.

Q6. Is ELSS the best tax saver investment plan in India?

ELSS is widely considered the best tax saver investment plan india for investors willing to take moderate to high risk. It has the shortest lock-in (3 years), highest return potential (10–15% historically), and qualifies for Section 80C deduction. However, for those seeking guaranteed returns, PPF or NSC may be more suitable.

Q7. What are the ways to save tax in India beyond Section 80C?

There are several effective ways to save tax in india outside of 80C:

- Section 80D: Health insurance premiums

- Section 80E: Education loan interest

- Section 80G: Charitable donations

- Section 24(b): Home loan interest

- Section 80TTA/80TTB: Savings/FD interest for senior citizens

- Section 80CCD(1B): Additional NPS contribution

Q8. Which tax saving investment in India is safest?

The safest tax saving investments in india are government-backed instruments: PPF, NSC, Sukanya Samriddhi Yojana, and Senior Citizen Savings Scheme (SCSS). These carry zero default risk, offer guaranteed interest rates, and fall under Section 80C.

Q9. Can I invest in multiple tax saving investments in India simultaneously?

Absolutely. Investing in multiple tax saving investments in India across 80C, 80D, NPS, and home loan interest is not only permitted but recommended. Diversification across PPF + ELSS + NPS + health insurance ensures you maximize deductions while balancing risk and returns.

Q10. When should I start investing in tax saving schemes in India?

The best time to start tax saving investments in india is the beginning of the financial year — April 1. Early investment means more months of compounding, lower monthly SIP amounts for ELSS, and no last-minute panic purchases. Starting a PPF or ELSS SIP in April is one of the smartest ways to save tax in india that most financial experts recommend.